References

- Rashbrooke M. Reforming Income Tax: Tax Justice Aotearoa Policy Brief Four. Wellington: Tax Justice Aotearoa, June 2020. Accessed August 27, 2020. https://taxjustice.nz/wp-content/uploads/2020/06/Reforming-Income-Tax-TJA-Policy-Brief-Four.pdf

- Fyfe J. Coronavirus and social inequality: How poorer Kiwis are set to bear the brunt of COVID-19. Newshub 2020 April 2, 2020. Accessed August 20, 2020. https://www.newshub.co.nz/home/new-zealand/2020/04/coronavirus-and-social-inequality-how-poorer-kiwis-are-set-to-bear-the-brunt-of-covid-19.html

- Radio New Zealand. Women more vulnerable to job losses, commissioner says. Wellington: Radio New Zealand, August 6, 2020. Accessed August 20, 2020. https://www.rnz.co.nz/news/national/422872/women-more-vulnerable-to-job-losses-commissioner-says

- Salvation Army Social Policy & Parliamentary Unit. COVID-19 Social Impact Dashboard 9 April 2020. Auckland: Salvation Army (New Zealand), April 9, 2020. Accessed August 20, 2020. https://www.salvationarmy.org.nz/sites/default/files/uploads/2020/March/sppu_covid-19_update1.pdf

- Kaye-Blake B. Targeting support for rural communities in the COVID-19 recovery. Wellington: NZIER, May 2020. Accessed August 20, 2020. https://nzier.org.nz/static/media/filer_public/ab/d8/abd8616a-287a-42c1-95e7-fe7fe6b08ca0/nzier_insight_86-2020_targeted_support_for_rural_communities.pdf

- Wilson N, Boyd M, Kvalsvig A, et al. Public Health Aspects of the Covid-19 Response and Opportunities for the Post-Pandemic Era. Policy Quarterly 2020(3):20-24.

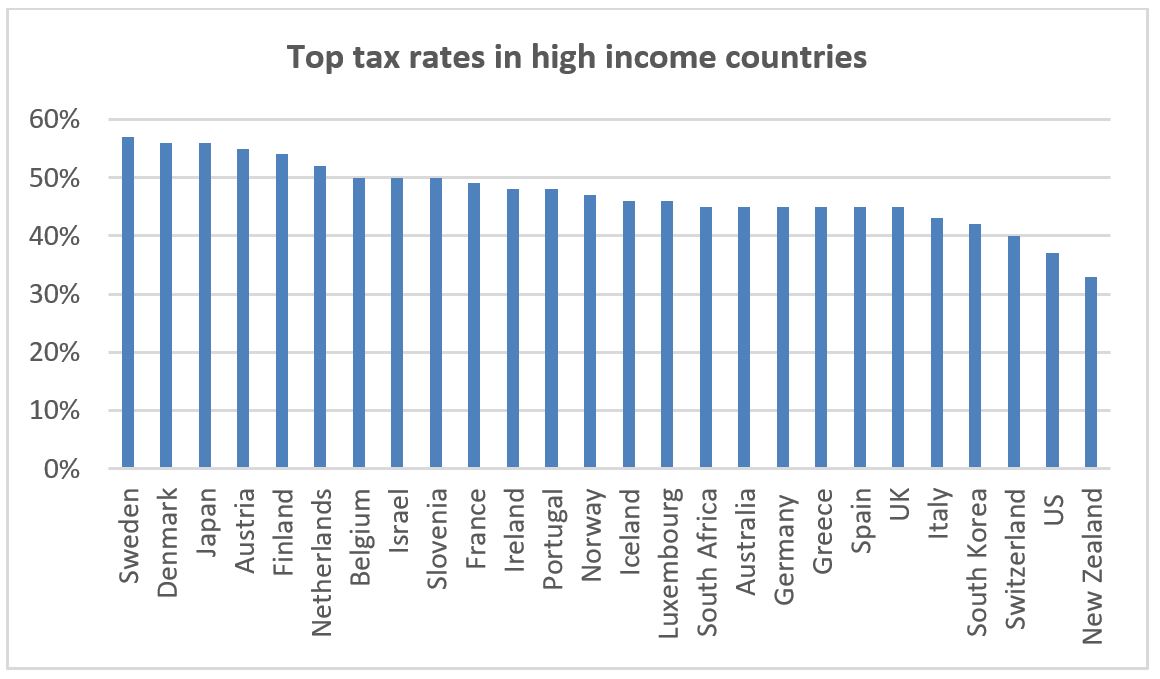

- OECD. Revenue Statistics 2019. Paris: OECD, 2019. Accessed August 27, 2020. https://www.oecd.org/tax/tax-policy/revenue-statistics-highlights-brochure.pdf

- NZIER Public Good Team. How do we pay for the Covid-19 stimulus package? Auckland: The Spinoff. Accessed August 27, 2020. https://thespinoff.co.nz/society/nzier/17-04-2020/how-do-we-pay-for-the-covid-19-stimulus-package/

- Burton T. Tony Burton reminds us that while Covid-19 loads us up on public debt, there is little that is ‘kind’ about repaying debt. Auckland: interest.co.nz, May 31, 2020. Accessed August 27, 2020. https://www.interest.co.nz/opinion/105297/tony-burton-reminds-us-while-covid-19-loads-us-public-debt-there-little-kind-about

- Victoria University of Wellington Tax Working Group. A Tax System for New Zealand’s Future. Wellington: Victoria University of Wellington, January 2010.

- Pullar-Strecker T. Capital gains tax abandoned by Government. Stuff 2019 April 17, 2019. Accessed August 20, 2020. https://www.stuff.co.nz/business/112010254/government-to-make-statement-on-capital-gains-tax

- Inland Revenue. Tax rates for individuals. Wellington: Inland Revenue,, August 2020. Accessed August 20, 2020. https://www.ird.govt.nz/income-tax/income-tax-for-individuals/tax-codes-and-tax-rates-for-individuals/tax-rates-for-individuals

- Lawton K, Reed H. Property and wealth taxes in the UK: the context for reform. London: Institute for Public Policy Research, March 2013. Accessed August 27, 2020. https://www.ippr.org/files/images/media/files/publication/2013/03/wealth-taxes-context_Mar2013_10503.pdf

About the Briefing

Public health expert commentary and analysis on the challenges facing Aotearoa New Zealand and evidence-based solutions.

Subscribe

Public Health Expert Briefing

Get the latest insights from the public health research community delivered straight to your inbox for free. Subscribe to stay up to date with the latest research, analysis and commentary from the Public Health Expert Briefing.