Last month the British Medical Journal published a study on the highly anticipated purchasing data examining the impact of taxing sugar sweetened beverages (SSB) in Mexico (1). This study reported that the 10% tax on SSBs was associated with an overall 12% reduction in purchases and a 4% increase in purchases of untaxed beverages one year after implementation. In this blog we examine this latest study, how it fits in with existing evidence, and how these results might apply to improving the control of obesity and improving child oral health in New Zealand.

From 1 January 2014, Mexico implemented an excise tax of 1 peso per litre on sugar sweetened beverages. These findings deserve to be looked at carefully given the growing international interest in taxing unhealthy foods. SSB tax is recommended by the final report from the Commission on Ending Childhood Obesity (ECHO) published 25 January 2016 (2), as one of a range of measures to address the environment causes of overweight and obesity requiring greater political commitment.

How was the Mexico study done?

The study addressed a clearly focused question; to evaluate changes in the purchases of consumer beverages after the implementation of the excise tax by using scanned and recorded individual food purchase data (Nielsen Mexico Consumer Panel Service).

The SSBs that were taxed included carbonated fizzy drinks and non-carbonated SSBs such as flavoured water and sweetened fruit juice. Untaxed beverages were carbonated drinks such as diet fizzy drinks; sparkling, still, or plain water; and other drinks, including unsweetened dairy beverages and 100% fruit juices with no added sugar.

The study was urban based. A representative group of Mexican households was recruited and then followed up from January 2012 through December 2014. The eligible population represented 63% of the Mexican population (i.e., those living in cities with more than 50,000 residents) and 75% of food and beverage expenditure. The authors weighted the results for household composition, locality and socioeconomic position to match demographic estimates.

Because of seasonal (more SSBs drunk in Mexico in summer) and long-run trends in SSB consumption (e.g., a pre-tax trend of decreasing consumption levels for reasons other than tax), it is vital that an analysis of SSB tax impact compares post-tax consumption with what consumption would have been based on past trends continuing – not a simple before-after comparison. Therefore the authors modelled a counterfactual consumption as though the tax had not been imposed. Specifically, they used a pre post quasi-experimental approach using “difference-in-difference analysis” and a “fixed effects model” that has the advantage of accounting for non-time varying unobserved characteristics of households (for example, preference for certain types of beverages). The model also adjusted for time varying confounders: unemployment rates and minimum income levels. However, it was not possible to adjust for changes in health promotion activities that could also have changed SSB consumption. For example, there were health campaigns about sugary beverages, anti-obesity programmes and economic changes occurring simultaneously that were unable to be accounted for.

What were the results in more detail?

The 10% tax on sugar sweetened drinks in Mexico was associated with a 12% reduction in purchases of drinks included in the tax, and a 4% increase in purchases of untaxed beverages a year after implementation. The impact increased over time and the most disadvantaged groups had the greatest reduction in SSB consumption. The tax was considered to be ‘pro-equity’ as would be expected given the evidence that lower income people are more price sensitive (see blogs from 2013 and 2014). This matters because SSB consumption, obesity, diabetes and other non-communicable diseases (NCDs) are strongly socially patterned. A greater impact on consumption in the most disadvantaged groups leads to greater potential health gains in these groups and greater health inequality reduction.

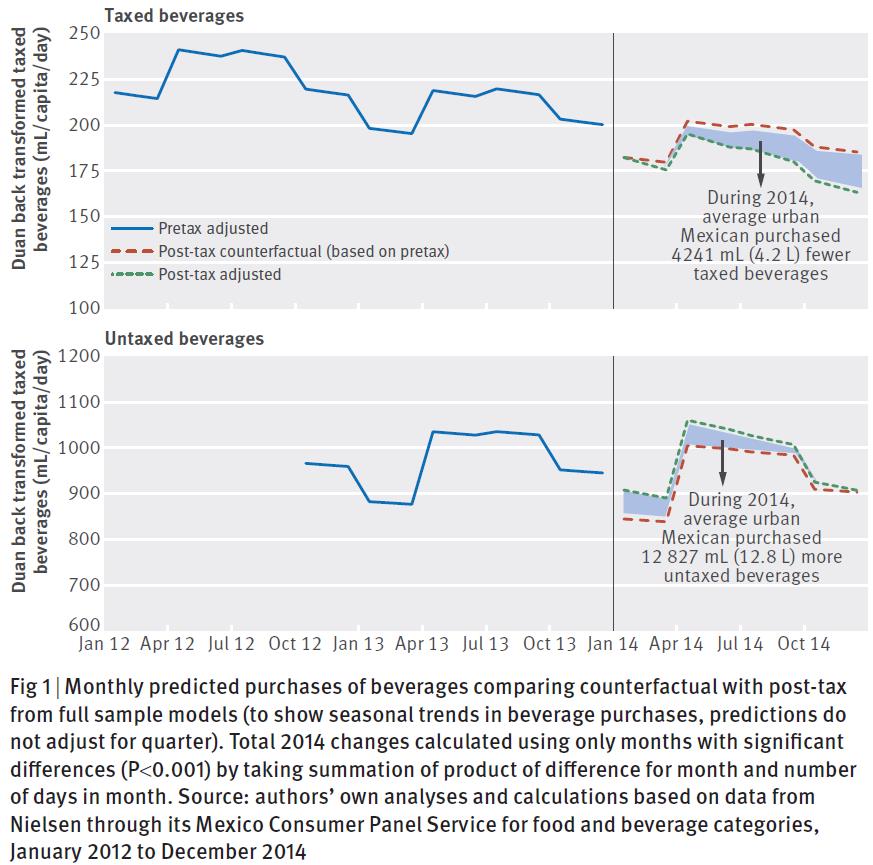

Figure 1 from the study in the BMJ (1) shows the volume of consumption tracking over time for taxed SSBs (top) and untaxed beverages (bottom). At the beginning of 2014 a red line shows the modelled consumption expected without the tax (counterfactual). The green line shows the observed beverage consumption, and how on average, a person living in a Mexican city purchased 4.2L less of taxed beverages.

The differences between observed consumption and the counterfactual were highly statistically significant – it was after all a large sample. So the findings are almost certainly not due to ‘chance’. The main remaining source of bias, though, is the inability to control for time-varying confounding – especially changes in health promotion and the level of industry promotion of SSBs. The authors appropriately suggest that more work is needed here. However, by using the counterfactual approach – of estimating what consumption would have been in the absence of tax – trends in consumption that reflect trends or ‘ongoing levels of other drivers influencing SSB consumption’ are probably taken into account. Put another way, as long as the net impact of health agency and industry activity to (dis)encourage SSB consumption was much the same before and after tax, the results should be valid. Our assessment is that potential residual confounding that might overturn this study’s main findings is unlikely (though it cannot be ruled out). Furthermore, health campaigns introduced in conjunction with a tax can be a valid option from a public health perspective (if cost-effective), as these may strengthen the impact of a SSB tax on reducing consumption and optimise public acceptability.

The results of this study are consistent with modelling (3) (see a previous blog on Australian modelling), beverage sales data (4-6), and pricing data. Pricing studies have demonstrated how the SSB tax was passed along to consumers for all SSBs and for carbonated SSBs the extra price consumers paid after the tax was introduced was more than the 10% tax introduced (over-shifting) (7). Study results are also consistent with the very well established results internationally for other health-related taxes on tobacco and alcohol. Further monitoring in Mexico and case studies from other countries would further inform the evidence around SSB taxation and clarify the long-term impact of the tax, potential substitutions and its overall health implications.

How might the results apply to New Zealand?

New Zealand has some of the highest adult obesity rates in the OECD (at 31%), like Mexico (at 32%). Furthermore, both SSB consumption and obesity are strongly socially patterned, suggesting greater potential benefit from SSB taxes for those with the greatest rates of obesity-related disease. Mexico has introduced a wide suite of interventions that are expected to work together to reduce SSB consumption; including restricted sales of calorie-dense foods in schools, limited airtime for junk food advertisements on children’s TV programmes, and a special tax on packaged snacks. We suspect that introducing a SSB tax could be an important component of a comprehensive government strategy to help fix the obesogenic environment in New Zealand and to also improve oral health for both children and adults. Such a tax could complement policies to restrict sales of calorie-dense foods in schools and to restrict junk food advertisements to children on all media as recommended in the ECHO Report. The extra tax revenue could be used to fund child health initiatives such as expanded fruit provision in schools, provision of healthy school lunches, or expanded dental services (see a previous blog on SSB tax implementation) as has been done in other settings.