There are many ways that taxes on sugar-sweetened beverages (SSBs) can be designed and implemented. These aspects can affect the likely impact on SSB consumption and health. This blog looks at a policy discussion document from the Pacific and explores some of the reasons SSB tax outcomes from Mexico appear to show positive reductions in SSB consumption.

SSBs are defined as any beverage that contains added caloric sweetener usually sugar. The main categories of sugary drinks include soft-drinks/fizzy-drinks, sachet mixes, fruit drinks, cordials, flavoured milks, cold teas/ coffees, and energy/sports drinks (New Zealand Beverage Guidance Panel, 2014).

Pacific findings

The Pacific Island Countries and Territories (PICTs) account for many of the highest rates of obesity and diabetes in the world. The Secretariat of the Pacific Community policy discussion document published early in August 2015 (McDonald, 2015), outlines several important messages about sugar sweetened beverage (SSB) tax and other regulatory measures from the Pacific.

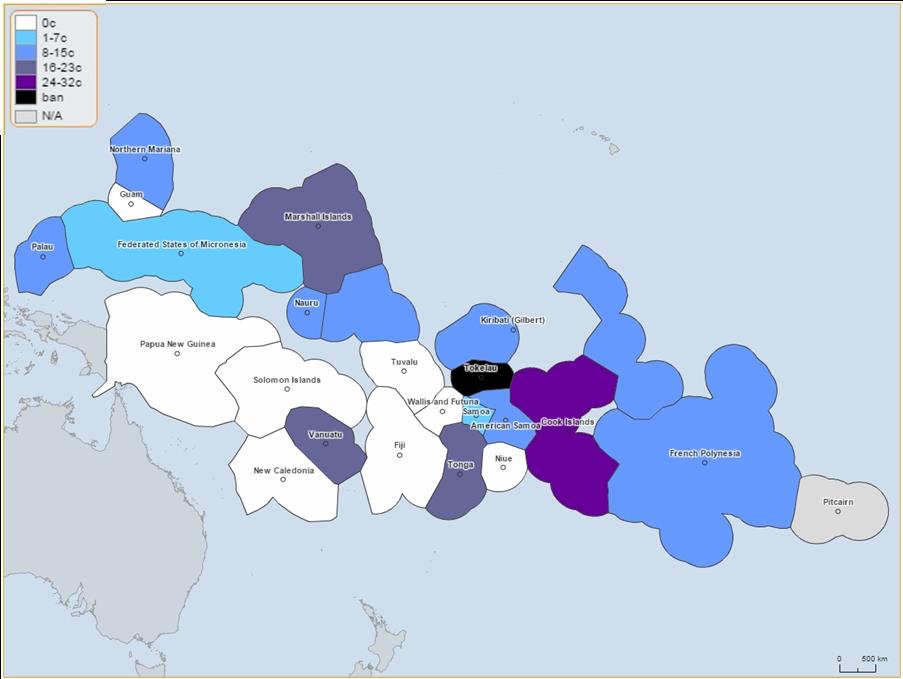

- Already half PICTs have implemented a tax on sugar drinks, over and above the tax on other food and beverages (Figure 1). In April 2014 the Cook Islands adopted a NZ$9.80 tax per kg of sugar on sugar sweetened soft drinks which is equivalent to NZ$0.38 additional cost for a can of coke. In the Pacific this was the highest value of SSB tax known to date.

- The effectiveness of SSB taxation in improving health outcomes depends on how the SSB tax is designed including communication of a clear health goal, using excise tax, taxing on volume or sugar content, taxing a broad range of SSBs, introducing an adequate tax rate (e.g. 20+%), investing revenue back into health, and ensuring affordable healthy alternative beverages. The Pacific provides a wide range of SSB tax examples including revenue gathering aims rather than health (Fiji), under-shifting of SSB tax with introduction of cheap SSB imports (Nauru), differential taxes on imports and locally produced SSBs (French Polynesia), and a specific tax on sugar in SSBs (Cook Islands).

- Tokelau, a small island state of 1600 people, banned sugar sweetened soft drinks altogether since 2009 on one atoll and then subsequent atolls, with a significant drop in SSB importation and consumption (Rush, Pearce, & Drewnowski, 2012). Other small island developing states may have the ability to take the same community led action based on a serious consideration of the research, harms and potential benefits.

Figure 1: Typical level of sugar-sweetened beverage tax (USD) on a 355 mL can of coke in Pacific Island Countries and Territories, over and above tax levels applied to other foods and drinks, 2014.

Note: Ad valorem taxes in Nauru, Federated States of Micronesia, and Kiribati are calculated based on a US$1 price for a can of Coke. Tokelau has an import ban on carbonated soft drinks but no soft-drink tax. © Secretariat of the Pacific Community (2015)

Mexico

Similar to the Pacific, Mexico has some of the highest rates of obesity and SSB consumption rates (e.g. 163 L/person/year). Mexico introduced a 1 peso per litre SSB tax on 1 January 2014. So how did this tax stack up in terms of the design and implementation issues discussed above?

- Was a clear health goal communicated? – Yes, the expressed aim of the soda tax was for discouraging sugary drink consumption due to its negative effects on health. Nearly everyone who participated in an August 2014 survey (98%) said they considered drinking soda raises their risk for developing diabetes and obesity.

- Was it an excise tax? – Yes. Excise taxes apply to both local production and imports and can be designed to be consistent with trade agreements, whereas import tariffs are frequently subject to trade agreements. Implementation of excise taxes can be more efficient if modelled on existing tobacco excise.

- Did the tax specifically target SSB volume or sugar content (rather than just value)? – The tax was applied by volume of beverage. This is likely to be more effective at reducing consumption than taxing on dollar value. The impact of a volumetric tax is independent of price reductions, does not have a diminishing effect on bulk purchases, and is less likely to encourage consumers to switch to less expensive brands than a tax on value.

- Did the tax apply to a broad range SSBs? – Yes, the tax included all non-dairy and non-alcoholic beverages with added sugar including juice. (It also added an 8% tax on high-calorie snacks, like potato chips and cookies.)

- How big was the tax? –The tax rate was 1 peso (USD 0.08) per litre, equivalent to approximately 10% of the price. There have been calls by public health advocates to increase the tax to 20% (Alianza por la Salud Alimentaria, 2015).

- Was revenue invested back into health? – Partially. The Mexican Government promised to ensure there is free drinking water in schools and to introduce other anti-obesity measures and public health advocates say that the program has been slow to get off the ground (Alianza por la Salud Alimentaria, 2015). The Finance Ministry calculated that the beverage tax would raise close to $1 billion of revenue in its first year. Meanwhile, the Government plans to allocate around $100 million to install water fountains in public schools this year, about a third of the annual amount originally estimated to complete the installations within three years (Guthrie, 2014).

- Did the government ensure affordable alternatives? – Partially. For example, the initiatives for water fountains in schools (discussed above). However, a proportion of the population has no access to drinkable tap water, without considering the quality (Guthrie, 2014). There remain calls to remove VAT from water <20L containers (Alianza por la Salud Alimentaria, 2015).

- Is the impact on consumption and health monitored? – Yes, several reports have been released.

It is clear that Mexico’s SSB tax was introduced using many of the evidence-based recommendations for designing a SSB tax for the greatest health impact. We would therefore expect the tax to have a significant impact on SSB consumption, and health gains over the long-term. Early empirical evidence emerging from Mexico shows significant reductions in SSB consumption. Mexico provides real world evidence that – so far – backs up modelling predictions, including that the outcomes of SSB taxation are most beneficial for the most deprived populations (as discussed here, June 2014).

Preliminary results, for example, on the impact of Mexico’s SSB tax on household purchasing of beverages in 2014 have been released by a research team at Mexico’s National Institute of Public Health (INSP) and the University of North Carolina (University of North Carolina Food Research Programme & Instituto Nacional de Salud Publica, 2015). The major findings from the study show that after introduction of a 1 peso per litre tax on January 1st 2014, (and adjusting for pre-existing downward trend and macroeconomic variables that can affect purchases);

- there was a 6% average decline in purchases compared to pre-tax trends, accelerated over the year to reach 12% by December 2014,

- all socioeconomic groups reduced purchases of taxed beverages,

- reductions in consumption were greater among lower socio-economic households, averaging 9% decline over 2014 compared to pre-tax trends, and up to a 17% decline by December 2014

- the expenditure on SSBs was lower in lower socioeconomic households than before the tax

- a roughly 4% increase in purchases of untaxed beverages over 2014, mainly driven by an increase in purchased bottled plain water

These results are consistent with other data sources on declining soft drink sales in Mexico and self-reported reductions in consumption of sugary drinks in 2014 (Guthrie, 2014). It remains to be corroborated by national sales data.

Possible implications for New Zealand

New Zealand too has one of the highest obesity rates in the OECD. Obesity is a complex problem and so efforts to tackle obesity should be multifactorial and include regulatory approaches. SSB tax is likely to be particularly useful as one component of a package. SSB tax is also one of the most cost-effective tools with little or no cost to the tax payer for the health benefit gained. Indeed, there are potential savings to tax payers if the SSB tax revenue is used to fund programmes such as healthy school lunches in deprived areas and (probably more important in absolute dollar terms) savings to the health system via reduced hospitalisation and other costs. A recent McKinsey report on NCDs, outlines that although evidence may be sparse in some areas there is certainly enough evidence to act, including using regulatory options and ongoing monitoring and flexibility over time (McKinsey Global Institute, 2014). So perhaps NZ needs to start having a mature public discussion about adopting a SSB tax – while continuing to learn from other countries and continuing to perform its own research on the likely benefits and risks.

Previous Public Health Expert blogs on SSB taxes

June 2014 – Would a sugary fizzy drink tax reduce health inequalities? Probably Yes

February 2014 – Taxes on fizzy drinks in NZ: preventing premature deaths and raising funds for health